The mobile industry is quickly preparing to incorporate satellite direct-to-device (D2D) or direct-to-cellular (D2C) services into their current mobile offerings. The prospect of ubiquitous coverage offers many benefits. Mobile operators would not have to spend on building and maintaining infrastructure and allocating spectrum to rural areas and hard-to-cover urban and suburban regions. They can avoid the costly and time-consuming process of obtaining permits for installing and improving cell towers. Such coverage would also open up more revenue opportunities in agriculture, mining, and logistics. Public safety and disaster preparedness is another key feature that can drive incremental revenues for mobile operators, both terrestrial and satellite. Currently, operators are introducing the concept of such coverage as an add-on feature to current cell phone plans and could generate a significant revenue bump for operators.

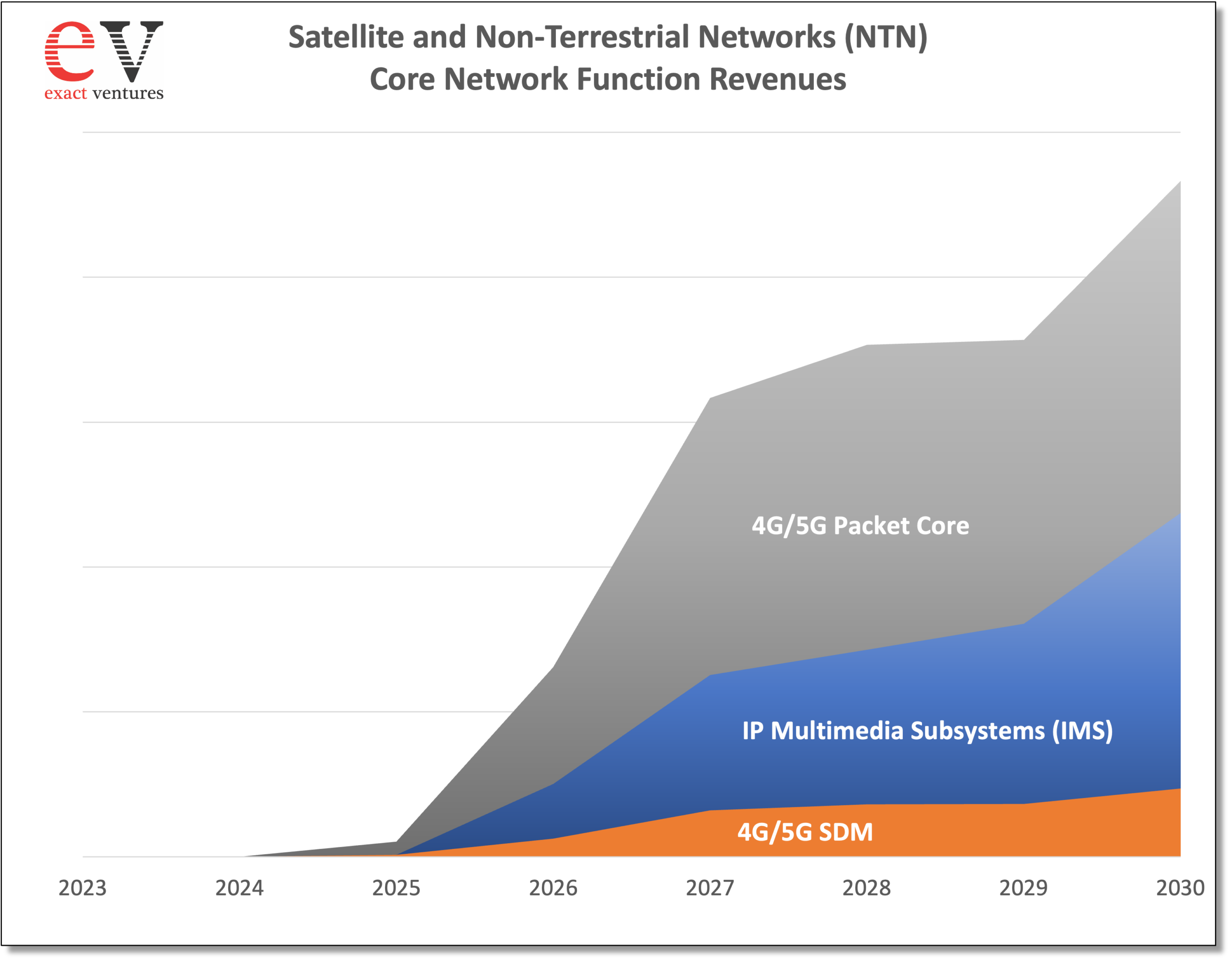

Specifically, we look at four segments: 4G Packet Core (supporting 4G LTE and 5G NSA access), 5G Packet Core (Supporting 5G SA access), 4G and 5G Subscriber Data Management (SDM), and IP Multimedia Subsystems (IMS) to support messaging and real-time communications services, like voice.

We use the following metrics the measure the various network functions that compose the Satellite or NTN Core market:

The network function vendors that are covered in the report, including vendor profiles include:

The satellite operators and service providers that are covered in the report, including vendor profiles include:

Please reach out (info@exactventures.com) for more details or for a table of contents for the report.