March 8, 2021, Burlingame, California, USA

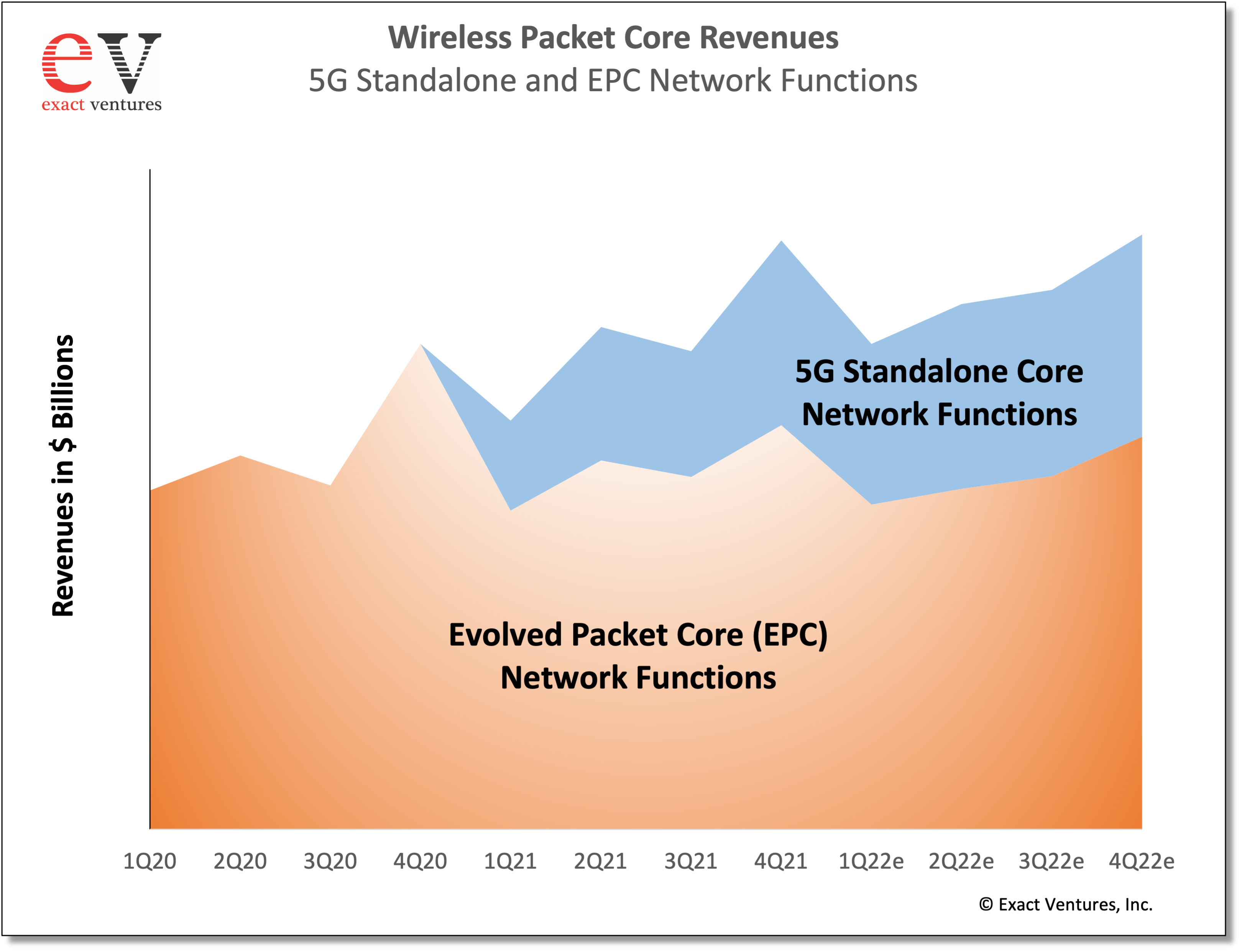

Exact Ventures recently reported that in 4Q21, the total 5GC and EPC market rose 23% sequentially to $803 million and the market was up 15% versus 4Q20, due to the inclusion and growth of 5GC revenues. In 4Q21, the EPC market grew 15% sequentially due to season spending patterns but was down 17% versus 4Q20 to $551 million and accounted for 69% of the market, with 5GC accounting for the remaining 31%. While other vendors have begun to recognize 5GC revenues, the market continues to be heavily dominated by Chinese operators and Chinese vendors as that country has been the most aggressive at investing in 5GC capacity to help support its 1.6 billion total subscriptions, over 40 percent of which (approximately 700 million) are currently 5G. Of course, such a quick buildup cannot continue, and we expect that other markets, and other vendors, will become a much greater portion of the market in 2022 and beyond.

For the full year 2021, the total (5GC + EPC) market grew 19% to reach $2.7 billion as the 5GC contributed $728 million and the EPC market fell by 6% to $1.7 billion. Much of the EPC market in 2021 and in ensuing year will be to support 5G NSA deployments which continue to leverage the EPC. The growth in 5GC revenues was due to China transitioning their spending faster than expected and is the reason for the increase in the market forecast. Since production SA core networks at scale are still limited to a very small number of network operators, shipments (and revenues) of 5G core network functions will be very volatile. 5G Core revenues are also likely to be highly variable due to complex and stringent revenue accounting and product acceptance criteria. There has also been some delay in some 5G deployments due to the pandemic slowing the standards process as well as slowing the testing and trial process. We forecast that the total market will increase by 8% for the full-year 2022 to $2.9 billion as growth in the 5GC market of 37% to $1.0 billion, helps to offset an expected decline in EPC sales. Nevertheless, EPC revenues are expected to contribute approximately two-thirds of the total packet core market for the year. Operators will continue to invest in the EPC networks for many years to support 5G via NSA network architectures, increases in usage, and to provide some level of feature parity and performance with 5G-SA based networks and services.

For more information or to purchase the report, please contact: sales@exactventures.com

Get in touch